Due to my need to sign up for insurances here in Germany (see car, legal expenses, etc), I asked myself:

“How do expats deal with that insurance topic?”

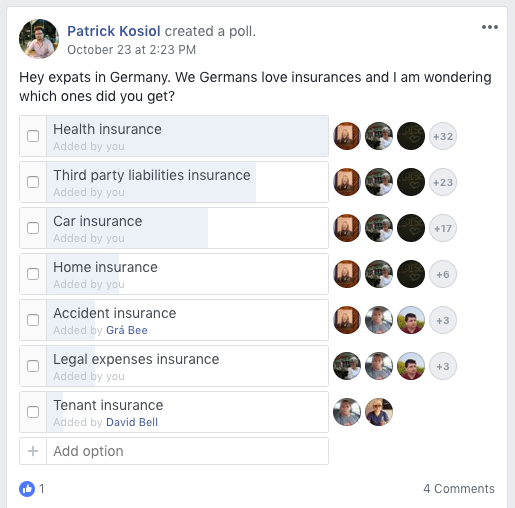

So I went out to two Facebook groups for expats in Germany and asked that question. These are the results I got:

In short, the three top most insurances are:

Health insurance

Third party liability insurance

Car insurance

I find it interesting that TPL is ranked second and car insurance is only ranked third. Perhaps some folks thought that I meant “Car TPL” with the TPL, which is the one that’s required by law. Anyhow, it’s still an interesting result, I find.

Personally, I don’t really like insurances and I try to avoid as many as possible. But Germans love insurances for some reason. I heard someone say a few years ago:

“If there would be an insurance for not having the right insurance, Germans would sign up for that.”

Perhaps that’s a market gap right there? 🙂

A good way to start looking for an insurance of any kind is Tarifcheck24. It’s a great comparison website for insurances and it’ll help you find the best deal.

To register a car – may it be a new one or one you bought second hand – you need to have at least a car insurance. Here is a quick overview of typical car insurances in Germany:

Haftpflicht = Third Party Liability (mandatory)

Like it is in many countries, it is required to have a third party liability insurance for your car in case you damage someone else’s car or hurt other persons with your car.

Teilkasko = Partial Comprehensive Cover (optional)

This optional insurance covers damages to your own vehicle to some extend. It makes sense to get this for some older vehicles that still have some decent value. For a car like ours, we did not opt for this.

Vollkasko = Full Comprehensive Cover (optional) This optional insurance can be signed up for instead of “Teilkasko”, which covers pretty much any kind of damage or loss at your car. “Vollkasko” makes sense for brand new and high value cars.

Hail Damage – Typical Damage Claim for a Comprehensive Cover Insurance

Finding the Best Car Insurance

There are many ways. Most folks would just ask their favorite insurance agent, but for me, I simply went on a price comparison website called Tarifcheck.de and searched for it.

To find the car insurance of your liking you need to:

Particulars of the car

Particulars of the holder/owner of the car and the driver(s)

Previous insurance coverage

Similarly to other countries, you’ll be classified into a “Schadenfreiheitsklasse” (SF) meaning you’ll get a “no-claims-discount” if you’ve got a good accident-free driving record. If you don’t have any record you enter the car insurance world with 100%-155% percent of the normal insurance rates. It can even go up to 245% for drivers with an extremely high record of accidents. For example, driving beginners that caused an accident themselves get put into that SF. So better drive properly and with care.

Here is a list of all such SF / no-claims-discount classes:

accident free years

Third Party Liability

Comprehensive Cover

SF-Class

Premium in %

SF-Class

Premium in %

Malus Class

SF M

245

SF M

160

Beginners

SF 0

230

SF 0

125

Special Class

SF S

155

—

—

Special Class

SF 1/2

140

SF 1/2

115

1

SF 1

100

SF 1

100

2

SF 2

85

SF 2

85

3

SF 3

70

SF 3

80

4

SF 4

60

SF 4

70

5

SF 5

55

SF 5

65

6

SF 6

55

SF 6

60

7

SF 7

50

SF 7

60

8

SF 8

50

SF 8

55

9

SF 9

45

SF 9

50

10

SF 10

45

SF 10

50

11

SF 11

45

SF 11

45

12

SF 12

40

SF 12

45

13

SF 13

40

SF 13

45

14

SF 14

40

SF 14

40

15

SF 15

40

SF 15

40

16

SF 16

35

SF 16

40

17

SF 17

35

SF 17

40

18

SF 18

35

SF 18

35

19

SF 19

35

SF 19

35

20

SF 20

35

SF 20

35

21

SF 21

35

SF 21

35

22

SF 22

30

SF 22

35

23

SF 23

30

SF 23

30

24

SF 24

30

SF 24

30

25

SF 25

30

SF 25

30

So if you’re accident free driving for 22+ years, you’ll get the lowest rates available.

If you sign up for a car insurance, it appears to be rather easy to claim your previous SF with the new insurer by simply entering it and providing your insurance account number of your previous insurance. If you are coming from a foreign country, you can try to get classified into a SF class according to your no-claim-record at your insurance. However, some insurers don’t accept that. Some might give you at least a bit of a discount. So I’d recommend to give it a try and check with a few insurers on whether they can accept your claim.

We’ve signed up for a third party liability insurance that costs us €247 per year where we got classified into SF15 that gives us 40% premium we have to pay. Without such SF classification we would have paid close to €600 per year instead. So it’s worth looking into that.

On the comparison website you can also see different ratings of such insurers. They tell you how well that insurer pays back claims, how responsive they are, whether they are environmentally friendly, do everything digitally, and so on.

Simply enter your car details and personal particulars there. You’ll then get a list of insurance offers. I for my part, signed up for the car insurance right on that website. It worked quite well for me, but feel free to consult other sources too.

My decision process was very simple: I took the insurance with the best combination of claim-refund rating, customer satisfaction and of course best-price. It turned out to be a small “direct” insurance company for me. That’s fine as I expect that we won’t be needing it — hopefully.